Oil and gas industries just enjoyed a bumper profit year, with shareholders seeing record payouts. In its wake, Europe’s Shell and BP both walked back on their ambitious low-carbon transition plans, with firms across the sector increasing their investing in new production.

That’s not good news for climate change, largely driven by burning fossil fuels. One worry is these investments mean the industry and its political allies will fight tooth and nail for them to avoid “stranded assets” losses, locking in higher production of climate changing fuels for years and even decades to come.

Not only the companies, but also their shareholders could turn, as vested interests, into a broad coalition against green energy. At least in the U.S. and the U.K., most pensions are invested in capital markets, where within stock markets oil and gas companies remain among the most reliable generators of dividends and share buybacks. All of this could deter governments from implementing all-too-ambitious climate mitigation policies for fear of causing financial losses to a broad swath of their own voters.

But based on a recent analysis, we argue that high-income governments need not worry about triggering these financial losses. That is because most hits from stranded fossil fuel assets—lower production volumes or sales at lower prices than investors expected—would fall primarily on the wealthy members of these countries. That ain’t most voters.

The explanation is relatively simple: these nations all have significant inequality in who owns companies. That means the wealthy generally own the vast majority of all stocks and bonds, and there is no evidence that differs significantly in the oil and gas sector.

Governments should indeed worry about potential effects on the users of fossil fuels, among car owners for example, caused by carbon prices and other climate policies that impose penalties on consumption, and there have been important proposals for measures to reduce the negative effects of fossil fuel phaseout on the most vulnerable people in society, such as “carbon dividends” and improved public transport. Governments should also worry about employees in the energy and other sectors and ensure a just transition for fossil fuel communities. However, for financial investments, the bottom 50 percent and even 90 percent of wealth owners could be compensated at very little cost compared to these other measures.

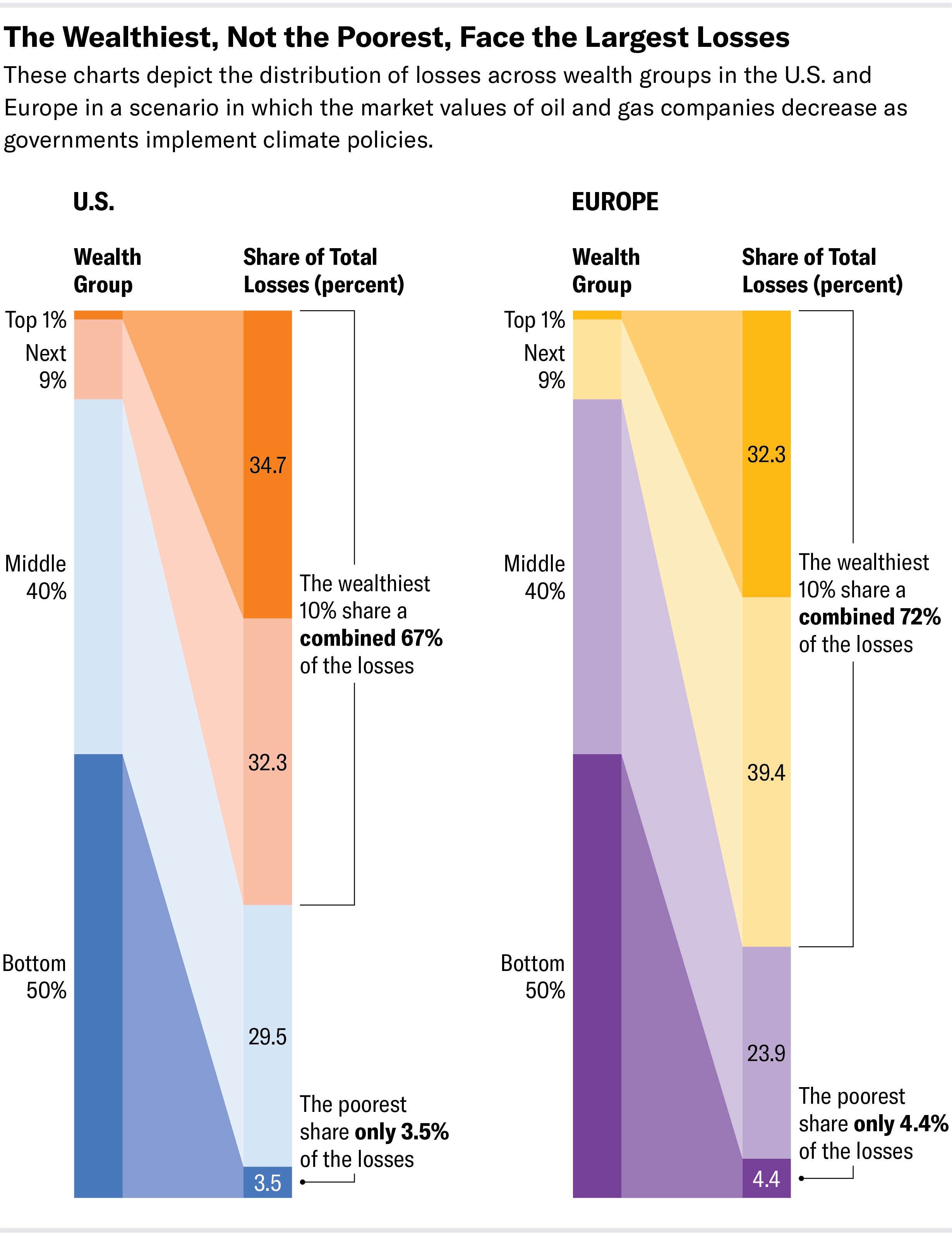

We have previously calculated that in a scenario where oil and gas companies are initially valued based on an expectation of participation in a growing oil and gas market, but governments around the world implement climate policies limiting global warming to 2 degrees Celsius above preindustrial averages, this could lead to wealth losses of nearly $550 billion for U.S. and European shareholders as companies’ market values are readjusted to these lower expectations. However, once we analyze where these shareholders are likely to sit in the wealth distribution, it turns out that only 3.5 percent in the U.S. and 4.4 percent in Europe of the losses harm the portfolios of the bottom 50 percent of them (see chart). Simply put, those who own most shares, also own most of the oil and gas sector shares that get devalued.

Because the top 1 percent and top 10 percent are so wealthy however (every U.S. American adult in the top 1 percent owns more than $13 million in net wealth on average) these losses, spread across individuals, hardly show in their portfolio. We estimate that losses amount to less than half a percent of the net wealth of wealthiest 1 percent or 10 percent of Americans, for instance. Moreover, as fossil fuels decline, new investment opportunities emerge in the growing markets for low-carbon alternatives that allow for portfolio hedging. Even losses for the least wealthy 50 percent and 90 percent are not high as a percentage of their wealth. The concern could arise from the fact that they have so little wealth in the first place. Compensating the bottom 50 percent would cost just $12 billion in the U.S. and $9 billion in Europe in a $550 billion loss scenario. This could be paid off with just one sixth of the annual revenue from a notional $13 per ton of carbon dioxide emissions price in the U.S., which is much lower than current consensus estimates of the social cost of carbon. In Europe, it could also be paid off with around 20 percent of the revenue from the European Emissions Trading System (ETS) in 2022.

One could argue that the rich are much more sophisticated investors and will get out of their investments before the shares lose their value, saddling the poor with much more of the losses. This is indeed a concern, yet our robustness calculations suggest that even if the poor were much more likely to own oil and gas shares, compensation costs would remain limited.

There are many obstacles to moving away from fossil fuels, from prices for consumers and firms to employment and meaning in communities where fossil fuel production is concentrated. Governments must address them all carefully. However, losses for financial investors don’t rank among them, and even if they were, we show that compensation for any socially relevant losses would be cheap indeed.

Warnings about pension losses and pushback against measures that would cause asset stranding appear largely made in the interest of the very wealthy, whose capacity to absorb losses is arguably much higher than everyone else’s. Losses from unmitigated climate change, on the other hand, will likely hit the poor and vulnerable much harder.

This is an opinion and analysis article, and the views expressed by the author or authors are not necessarily those of Scientific American.

{kind=link}